2018 will be the year for new investments in the O&G industry as crude oil prices are expected to be stabilize at $59 per barrel. Frost & Sullivan projects a 5% increment in upstream CAPEX in 2018 in tune with its recovery from 2017. In addition, the expected regulatory changes in Indonesia, Thailand and the technological developments in Malaysia are expected to boost tenders in the E&P sector. Operating costs for oil production varies by country in the APAC region. Hence, those countries with higher operational efficiency and higher production volume will attract greater investments.

Investments in coal power market in the APAC region will continue to dwindle for second year in a row, due to mounting challenges to get coal-fired power plants off the ground. Amongst the primary energy sources for power generation, coal will continue to be the least important in 2018 as focus will remain on renewables, mainly solar power.

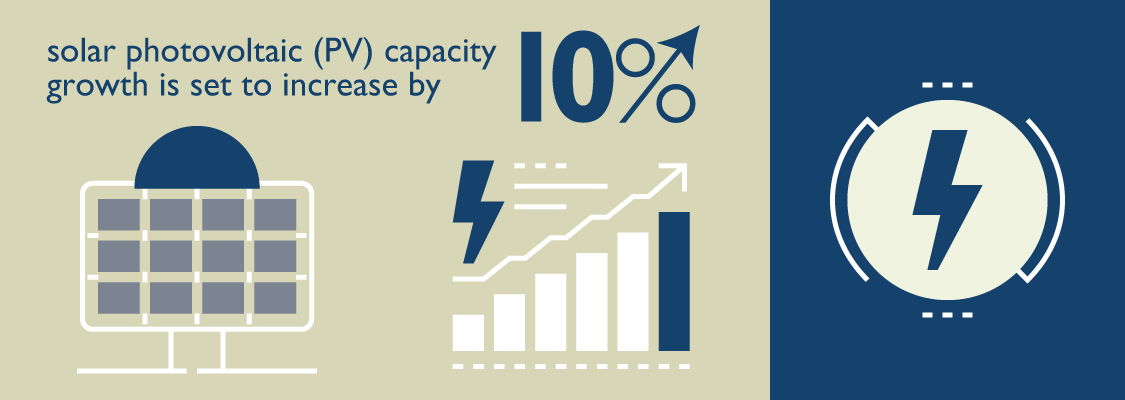

Fuelled by technology and business innovation, investments in renewable energy (RE) will continue their high growth trajectory. As countries transition to a low-carbon future, RE including hybrid projects will become a mainstream source of power. Annual solar photovoltaic (PV) capacity growth is set to increase by 10% in 2018 even as key markets such as India and Japan are likely to witness a slowdown this year.

2018 will see widespread investments in distribution grid management systems in Southeast Asian countries like Thailand and Vietnam. Utilities in Japan and Australia will take their first steps towards Internet of Things (IoT) implementation in the power sector by adopting this technology for their generation and grid equipment. Implementation of energy management software and IoT will be the key focus areas in the grids sector. Increased retrofit into smart electricity meters will be inevitable.

With new partnerships and new market entrants, disruption in ESS competition will be intense in 2018. Battery-based ESS projects will also register significant growth, especially in China, Japan, India, and Thailand.

Digitalization initiatives will sweep through all segments of the building industry, including construction, building management systems (BMS), and FM. The focus will be on transforming buildings to become intelligent and cognitive. M&As and partnerships for vertical, geographic, and capability expansion will become commonplace in the Asian FM market as companies look to combat unconventional new entrants.

Water utility industry CAPEX will grow by 9.6% in 2018. Asian water utilities will leverage digital platforms to improve service and revenue collection. Smart cities’ vision fruition and the redevelopment of water services will also open up opportunities for smart meter solutions and IoT providers. Partnerships and collaborations between water companies will gain prominence during this year.